Real economy merry and bright?

We feel somewhat ambivalent heading into the holiday season. Economic fundamentals still look firm (for now). And the retail data, of vital importance to a consumer-driven economy, appears off to a good start. Although in-store foot traffic on Thanksgiving and Black Friday declined slightly versus last year, online sales on Friday increased and the outlook for Cyber Monday appears strong, with consumers likely to set a nominal record for purchases. We do not read much into the slight decline in foot traffic and continue to believe that the demise of retail real estate has become overhyped.

We emphasize that retail remains the property sector most dependent upon local factors (within a property’s trade area), resulting in the most variable property-level performance among major commercial real estate (CRE) sectors.

Broad, sweeping generalizations about retail make for incendiary headlines, but poor retail real estate strategies. Our forecast model suggests that overall holidays sales should grow by at least 5 percent versus last year. But we see risk to the upside – consumer sentiment remains high despite some recent market-related pullback, the labor market continues to tighten pushing up wage growth, and the recent pullback in oil prices should boost consumer spending. A robust holiday shopping season would boost the fortunes of retailers and retail real estate centers, though we concede that the importance of holiday sales to those fortunes gets overstated.

Public markets' troubles aren't out of sight

Markets, on the other hand, have been feeling downright Grinch-like in recent weeks. The equity market has declined roughly 10 percent from its all-time high back in September and fixed income markets have gyrated while also trending down. Despite the positive current environment, markets and prices take a forward-looking view and several factors are upsetting the market. Economic growth has passed its post-tax cut peak and is slowing domestically and globally. The Fed looks set to continue raising rates and the dollar has strengthened in recent months: higher interest rates and a stronger dollar should dampen corporate margins. Trade tensions have not abated and if tariffs rise on January 1 as many expect they will further increase companies’ costs. The combination of these factors indicate that earnings growth has also likely passed peak and is slowing. Seen from this perspective, the paradox of a strong economy and declining markets is just a misreading with markets looking toward future, not current conditions.

Expect increased volatility to continue while the markets digest these changing conditions over the next few months.

Trade heading for an unhappy New Year?

Speaking of trade tensions, we continue to believe that anyone expecting a grand détente between the U.S. and China on the sidelines of the G20 summit in Argentina at the end of this week will likely be disappointed. At best, we expect the meeting to put a damper on further trade tensions. But the U.S. and China remain too far apart on fundamental trade issues and we see little chance that these differences will be resolved in short discussions between the countries’ presidents. Risk to trade policy remains on the downside, if for no other reason than the impending increase on January 1 of tariffs on roughly $200 billion of Chinese imports (from 10 percent to 25 percent).

Trade barriers are clearly having an impact on companies, which could potentially alter supply chains if they remain in place long enough.

For now, we reiterate our view that the tariffs should only modestly impact the economy and industrial real estate, but downside risks remain should trade barriers increase.

Do you hear what I hear?

Several Fed speakers will present or sit on panels this week and commentators will closely parse all of their words. Vice Chairman Richard Clarida will discuss data dependency and monetary policy, a timely topic given the potential for slowing economic growth and volatile markets to impact Fed policy. Chairman Jerome Powell will talk about the Fed’s framework for monitoring financial stability. That topic should not directly address any of the market’s concerns, but the question-and-answer session provides on open forum for virtually any topic. And a few other regional Fed presidents will be speaking as well on various topics.

Thus far, we see no reason to expect the Fed to back away from a rate hike next month.

Fed prognosticators have recently been tying themselves in knots attempting to factor recent market and economic developments into their outlooks. We have yet to alter our view that the Fed will continue to tighten in 2019 but will keep a keen eye on data heading into the new year for any sign that the Fed might ease up on tightening relative to its current forecast.

What to watch this week

Consumer confidence for October, like consumer sentiment out last week, looks headed down slightly with market gyrations impacting consumers’ feelings. The second estimate for the real GDP growth for the third quarter should change very little, with an upside in business spending largely offset by more modest retail data. New home sales for October should reverse some of the decline from September, but the trend still looks downward with higher mortgage rates reducing affordability. We expect personal income and spending for October to remain healthy, but we foresee core personal consumption expenditures (PCE) falling back slightly.

What it means for CRE

The environment for CRE looks favorable heading into the final month of the year. While CRE has encountered its share of challenges this year, performance has held up well. We see little to disrupt that. While healthy holiday sales will likely not result in a surge in net absorption (they almost never do) they can help to firm up existing demand. Industrial real estate remains at risk from trade policy, but fundamentals remain stable for now. Net absorption for apartments tends to slow during the final quarter of the year due to colder weather, the holiday season, and children in school. We expect that pattern to hold this year. And office real estate continues to ease slightly, with the market appearing slightly past peak. Overall, a solid, if not spectacular, year for CRE will wrap up in December.

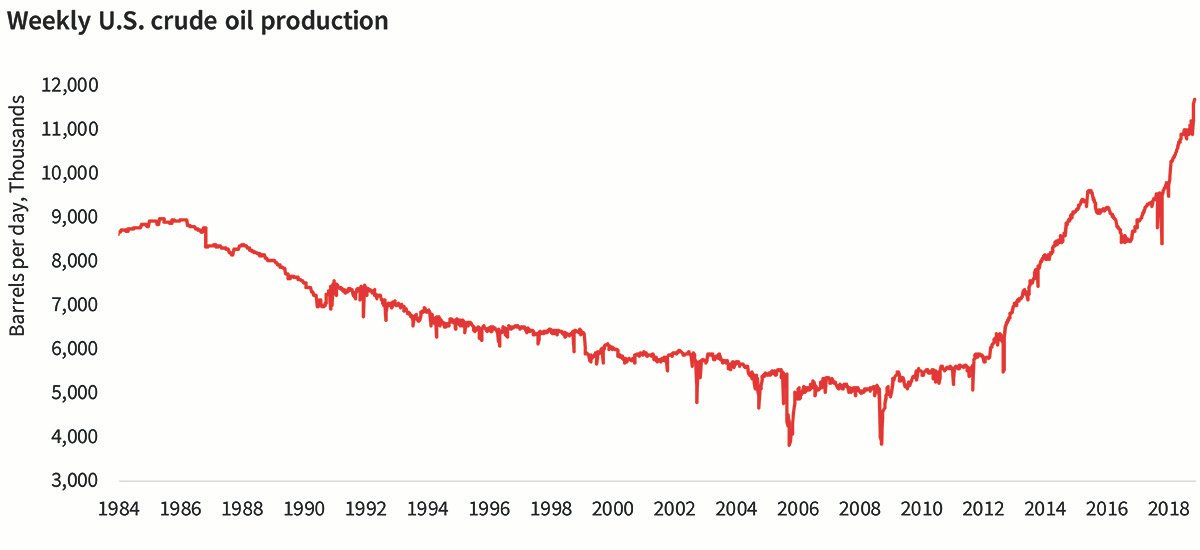

Thought of the week

U.S. weekly crude oil production is nearing 12 million barrels per day, up from less than 10 million per day a year ago and a low of roughly 3.8 million per day in 2005. The surge in supply, coupled with weaker demand, has caused crude oil prices to pull back sharply since a cyclical peak in early October.