Fiscal and monetary

policy take center

stage

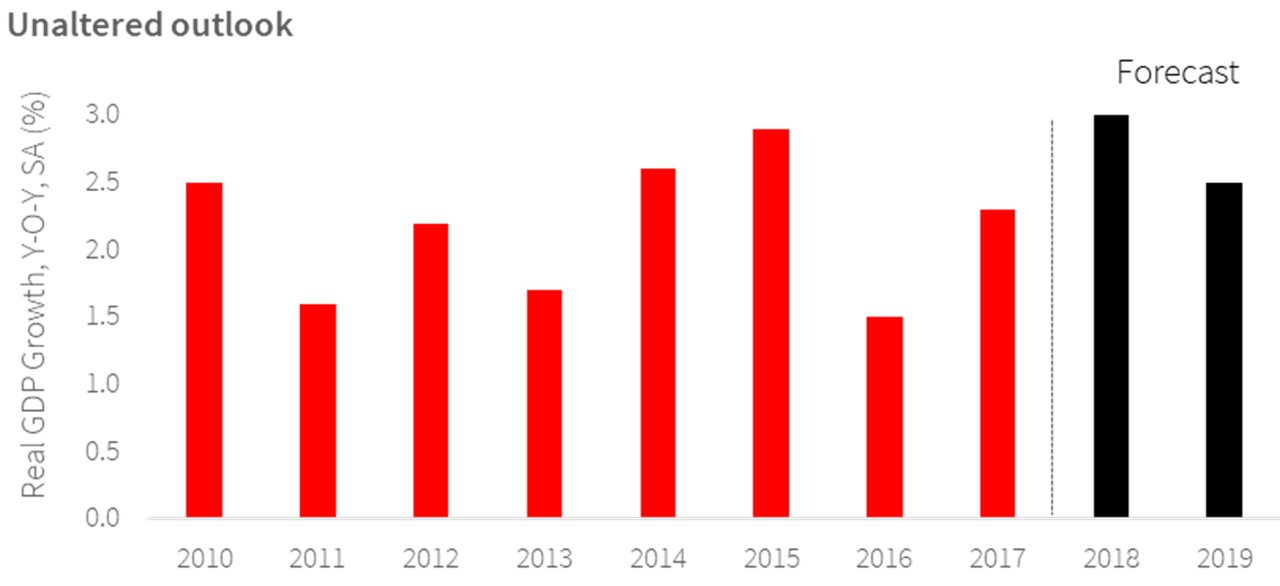

Two key events with significant policy implications came to the forefront last week. First, the midterm election produced the expected outcome with Democrats retaking the House and Republicans maintaining control of the Senate. The result produced a divided Congress that should not materially alter the trajectory of the economy. We published a more in-depth look last week, but the key development lies with fiscal policy. With the Democrats seizing control of the House, further tax cuts seem highly unlikely. The administration could work with the Democrats to pass an infrastructure spending bill, but whether this will happen remains uncertain because many Republicans will view an infrastructure bill as a non-starter due to rising debts and deficits. These developments do not alter our economic outlook from last week.

In short, we still see the economy growing around 3 percent this year and slowing near 2.5 percent next year.

Next year Congress and the administration will have to work together to pass some key initiatives: the new US-Mexico-Canada Agreement must get ratified, the debt ceiling needs to be raised by next summer, and a budget for fiscal year 2020 must pass.

Publicly-traded markets, which have gyrated lately, will view the removal of election uncertainty as a positive. The markets’ generally positive response to the election already shows signs of this. Typically, markets tend to perform well under divided government, but markets are also growing increasingly concerned about slowing global economic growth and earnings growth that now looks past peak, at least for several industries. We believe that the period of unusually low volatility in the markets has ended and that the news may more easily disturb the markets in future periods. |

Fed signals December hike coming, as we expected

Second, as we anticipated, the Fed did not raise interest rates last week, update its forecast (the dot plot), or hold a press conference. The Fed did release a statement indicating that recent market gyrations and tightening in financial conditions have not swayed its view on the outlook for interest rates. At this point a rate hike in December seems a near certainty, with the futures market pricing in a roughly 75-percent chance of an increase of 25 basis points. Attention now turns to 2019 and the trillion-dollar question of how many rate hikes next year.

Currently, we believe that next year the Fed will raise the fed funds rate by 25 basis points three times.

But we note that while consensus current sits in the 2-3 hike range, some economists are calling for as many as four. That seems a bit too aggressive for us given the current outlook on the economy, but if inflation surprises to the upside four rate hikes would not seem excessive.

Will business pass through rising costs?

Speaking of inflation, data from the producer price index (PPI) showed continued upward pressure, adhering to our medium-term forecast. The headline PPI exceeded expectations, with stronger wholesaler and retailer margins producing roughly half the gain.

This provides ample evidence that companies are pushing cost increases on to purchasers where they can to prevent margins from eroding.

This generates some upside risk to inflation. Meanwhile the core PPI, which excludes volatile goods like food and energy, inched upward as well, stabilizing over the past few months near 3 percent. Though just over four years old, the core PPI has reached its highest rate ever and looks to continue heading upward.

What else happened last week?

Key business and consumer sentiment indicators showed some slight softening, likely reflecting both the slowing in the real economy as well as the tumultuous markets. The ISM non-manufacturing index for October declined marginally while the preliminary reading on consumer sentiment for early November also pulled back a bit. Both remain at elevated levels, indicating a healthy expanding economy, but the ability of sentiment-based indexes to remain at or near record-high levels in the face of slowing economic growth will become more challenging over time. |

What we are watching this week

A busy week on the economic calendar starts with the consumer price index (CPI). Headline CPI should show an outsized increase for October, largely due to energy prices, reversing some slowing in the year-over-year change during recent periods. Meanwhile the core CPI should hold steady above the Fed’s target rate of 2 percent. Import prices for October should also show a modest gain, slowing a bit after a jump in September. We expect retail sales for October to grow by a healthy amount across both the headline and core categories, indicating strong momentum heading into the fourth quarter. A number of key Fed employees, including Chair Powell, will present, give Congressional testimony, or speak on a panel on a panel this week. While the markets will parse their words, we foresee no discernable impact on our forecasts.

What it means for CRE

Because the events of last week produced no meaningful change in our outlook for the economy, we see no meaningful change to our outlook for commercial real estate (CRE). We still foresee gradual increases in vacancy rates and gradual slowdowns in rent growth across the major property sectors over the next couple of years. Of note, in recent periods some signs of slowing have emerged in the industrial sector, the property type that had generally been performing the best in recent periods. If this anecdotal slowing becomes a trend (and only time will tell) that will likely push all four major property types past peak and signal an inflection point for this business cycle.

Thought of the week

The outstanding balance of leveraged loans (loans to highly indebted companies) now surpasses $1.1 trillion, a nominal record high and roughly double the amount from six years ago.

Please note: We will not publish Economic Insights next week due to the Thanksgiving holiday. Happy eating!