Too much of a good thing?

Data released over the last week reaffirms our belief in a strong U.S. economy that is pulling away from the rest of the world. But are we experiencing too much of a good thing? In the labor market the signs are pointing to yes.

The number of open but unfilled positions reached a record high of more than 7.1 million in August.

Since we wrote in depth on this labor shortage earlier this year, the number of open positions has increased by roughly 800,000. And rate of job openings (relative to the size of employment) also hit its highest rate ever. Increasingly workers are feeling emboldened, with workers quitting their jobs at a rate unseen since April 2001. What is motivating workers? In addition to the number of open positions, wage growth for job switchers has exceeded wage growth for job stayers throughout most of the current expansion.

Employers are increasingly compensating employees for staying in such a competitive environment. All of this is occurring in a market with a 3.7 percent unemployment rate (the lowest in half a century) that sits below estimates of the natural rate of unemployment of roughly 4.5 percent. Without a significant slowdown in job growth, which we do not foresee in the near future, the unemployment rate should continue to fall, fueling further wage gains. Unless we see significant revisions on prior periods or something truly idiosyncratic impacts the labor market this month, we expect year-over-year wage gains to finally top 3 percent in October for the first time during the current economic expansion and for the first time since April 2009. Wages look to make another jump, as we recently predicted.

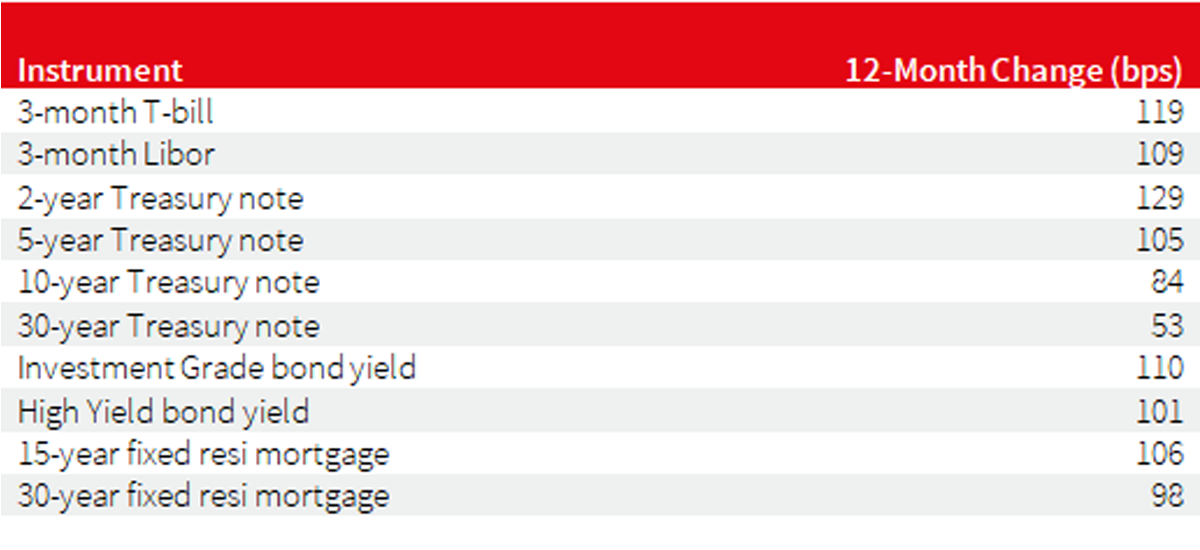

Workers are consumers too

While that all sounds great, it could present problems. As compensation increases employers will face a choice: raise prices for goods and services or suffer margin erosion. Typically, firms raise prices rather than suffer through margin erosion, declining stock prices, etc. Price increases put upward pressure on inflation, which has already been trending upward. And as inflation heads upward so do interest rates. Across instruments, we see that interest rates and yields have already risen by roughly 100 basis points (give or take) over the last year, and that even the yield curve has flattened. With the outlook for wage gains and inflation likely intensifying, we foresee more rate hikes from the Fed to the tune of one more this year in December and likely 2-3 more next year, raising the prospect of an inverted yield curve by the end of next year. Over the last 12 months, the Fed has hiked four times, 25 basis points each, compressing the yield curve (measured as the 10-2 Treasury spread) by roughly 45 basis points. Anything similar will certainly invert the 10-2 spread which currently sits just under 30 basis points.

Then why raise rates?

An inverted yield curve has historically predicted recessions quite well, which raises the question - why raise rates?

The Fed is trying to prevent the economy from running too hot, creating too much inflation, and risking a more severe downturn.

They are using higher rates to cool things off. They would ideally like to slow job growth, bring the unemployment rate up, tamp down inflation, and ease the economy into a “soft landing.” Thus far, their success in doing so has been mixed. The economy would likely run hotter without rate increases, risking letting inflation slip out of control and potential worse recession down the road. But even with ongoing rate increases, data last week showed that the economy continues to run hot. Consumers continued to spend money in September, particularly in the core retail sales category, which strips out some volatile components. And businesses continued to look healthy: inventories grew as expected in August and industrial production for September exceeded expectations. All of this bodes well for GDP growth in the third quarter, but do we need such strong growth? Would lower growth be better – remember our Goldilocks economy of the last few years?

What we are watching this week

The first estimate of annualized real GDP growth for the third quarter should clock in above 3 percent. While that represents a slowdown from second quarter’s 4.2 percent annualized rate, it sits well above the economy’s long-run potential of closer to 2 percent growth. And we see strong momentum heading into the fourth quarter thus far. Growth of this caliber should continue to drive job gains, wage growth, inflation, and interest rate increases.

Economic growth will slow once the fiscal stimulus fades, but that should not occur in earnest until the latter half of 2019 at the earliest.

We will also closely watch new home sales. Housing market data has trended weaker in recent months – existing home sales, starts, and permits. We will look to see if new home sales can buck the trend, though higher mortgage rates will challenge the market.

What it means for CRE

For commercial real estate (CRE), the issue now becomes one of the short run versus the medium run. In the short run, all of this looks good. A strong economy generates demand for CRE across the major property types. For retail in particular the current environment looks solid with strong consumer spending driving the economy. But where does all of this lead? Keep following the trends, be diligent, and avoid complacency. Taken to the logical conclusion, even if the economy skirts a technical recession, slower economic growth and higher interest rates will present a more challenging market environment for CRE, one characterized by higher vacancy rates, slower rent growth, and even rising cap rates. We are certainly not rooting against a strong economy, but we are also not ignorant of the challenges that will likely arise from one either.

Thought of the week

As the trade war with the U.S. intensifies, China is feeling the impact – economic growth is slowing, the yuan has fallen versus the dollar, and the stock market is declining. In response to these changes, China is currently the only major economy loosening monetary policy.